Jeremy Towler, senior market intelligence consultant at BSRIA, focusing on Building Automation and Control Systems in the “Smart Systems” team, takes a deep dive into the BACS industry.

The Building Automation and Control Systems (BACS) industry first emerged in the western hemisphere, and the leading incumbents are the same companies that established themselves early-on in those markets. Today, 4 companies account for around 54% of the world market – adding a fifth company takes it to just over 60%. Of those, 3 were founded in the USA, and 2 were founded in Europe – one German and one French.

Western countries mostly still account for the lion’s share of the world market too. In 2023, the USA was the largest single market, representing around one third, Germany ranked second at almost ten percent, and China a distant third at less than half the size of the German market. Meanwhile, due to a significant contraction of the Chinese market in 2024, France and Canada have edged ahead into third and fourth positions respectively, and China has fallen back to fifth position.

From a regional perspective, the Americas and Europe are practically identical in size in 2024 at around 38% each. The Middle East and Africa take less than 5%, however Asia & Oceania have grown incrementally over the years and now account for around one fifth of the world market.

So far, the emergence of new country markets to represent any significant scale, has been slow, and (with the exception of the rather insular Japanese market) most of the expertise for product innovation and market growth has remained in the west. However, countries such as China and India have the manpower and demand from major metropolitan conurbations to potentially develop their own BACS products in future, arguably at lower costs than their western competition, thereby opening up BACS to buildings that in the past could not have afforded it. Indeed, our research has revealed that steps have already been taken, with the development and production of field devices, such as valves and actuators in these countries.

BSRIA bases its 5-year forecasts on a combination of projections of GDP, new construction/ refurbishment, major project plans (such as Olympic Games, Football World cup etc.), legislation and market-player sentiment. What cannot be foreseen are natural catastrophes or pandemics, and the outbreak (or cessation) of wars and conflicts is hard to predict.

Forecasts in the latest BSRIA World BACS study were formulated largely based on data produced prior to the new USA Administration. Due to a range of factors, such as buoyant economic forecasts and legislation mandating the use of BACS in many commercial buildings, these suggest that by 2029, the USA will actually have increased its share by about 1.5 percentage points, whilst the shares of Germany and France remain broadly steady. Such was the fall in the Chinese market in 2024, that forecasts have suggested it will remain in fifth position up to 2029.

But as political and economic tectonic plates shift, is the status-quo about to be disrupted any time soon? Will the recent imposition of steep tariffs by the USA on its trading partners force those countries to focus their efforts elsewhere? Will those countries strengthen legislation on emissions and energy conservation, and ramp-up investment at home and in emerging markets in Asia and Africa? Many of these markets are very populous and theoretically offer enormous potential. And will it hasten the development of home-grown BACS products and solutions? If these trends gain traction, then the share taken by niche and emerging markets may quickly grow beyond the approximately 25% they represent today.

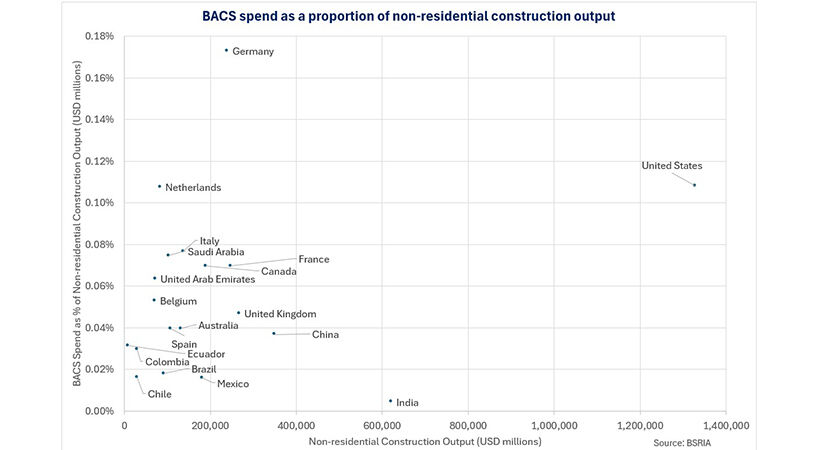

On the other hand, does size alone matter? Another way to analyse country performance and potential, is to compare the total BACS spend as a proportion of non-residential construction (NRC) output.

At 0.17% of NRC, Germany spends a higher proportion on BACS than any other country, significantly more than the USA at 0.11%, whose NRC is 5.5 times higher. By contrast, India spent just 0.0045% of its NRC output on BACS even though its NRC output was 2.6 times greater than Germany and nearly half that of the USA. It implies that buildings are for the most part, either being equipped with very rudimentary BACS, no BACS, or are using variable refrigerant flow (VRF) type cooling equipment with its own factory-mounted dedicated controls. China is spending a little over half that spent on NRC by India but is spending nearly 5 times more per capita on BACS, indicating that, by comparison it is a more mature market. Finally, the Netherlands spent the same proportion on BACS as the USA, despite US NR construction spend being 16 times greater.

Germany, France and the UK are each of a similar magnitude in terms of NRC output and yet France is spending a notably higher proportion on BACS than the UK, but Germany spends far and away the greatest proportion globally (0.173%), which reflects the high sophistication of its solutions and the high value placed on building automation and controls in general.

There is yet, another way of assessing the BACS market is to posit that the “richer” a country is in terms of GDP (per capita), the higher the spend per capita on BACS is likely to be. Analysis of the BACS markets recently surveyed does indeed suggest that there is a strong correlation (using NR construction produces a similar conclusion). Countries such as the USA, The Netherlands, Germany and the United Arab Emirates, which have a high average per capita GDP, have a high spend per head on BACS. Conversely, countries like China, India and Mexico have a lower per capita GDP and a much lower per capita spend on BACS.

This provides us with a useful metric to identify those markets which are relatively “mature” in that they have a high BACS spend relative to their GDP, and those which can potentially be seen as underdeveloped. The “mature” markets would include The Netherlands, Germany, The United Arab Emirates and Saudi Arabia. It suggests that the markets with a disproportionately low spend are under-developed markets. These include China, Spain, the UK, Australia and the USA.

Given that the USA is by a large margin, the largest BACS market in the world, this might seem surprising, particularly as the USA has the highest per capita GDP of any major economic power, but it shows that the country still has a lot of room for growth. There are clear opportunities in the lower income countries of China, India and South America, particularly in larger cities, where the demand for commercial real estate is highest.